When the Stars Fall #1- Innovative Food Holdings $IVFH

Written by Jochem Verzijl

Been thinking about how to start this new series of mine, but in the end the best learning curve is experienced by actually getting started. Let’s call this series 'When the Stars Fall’, a beautiful metaphor for what this series tries to accomplish hehe.

The goal of this series is to identify what variables cause a perfect setup to fail in microcaps. I think these case studies function as a perfect piece of information to understand business cycles better, and it might help investors recognise these situations in their own holdings, and hopefully help them act on it early enough.

Small sidenote: this is not meant as a dig into any investor who wrote up the names I am about to cover in this series. Everyone makes mistakes, and let's learn from them together

For this first edition of When the Stars Fall, I want to write about Innovative Food Holdings. In the early 2024’s, this microcap specialty food distributor and logistics provider looked like the perfect setup that makes every microcap investor’s eyes sparkle: asset-light with a competitive advantage, cheap, FCF-positive, an aligned management team incentivized to grow EPS at high digits. There was even a catalyst in play that could unlock major value.

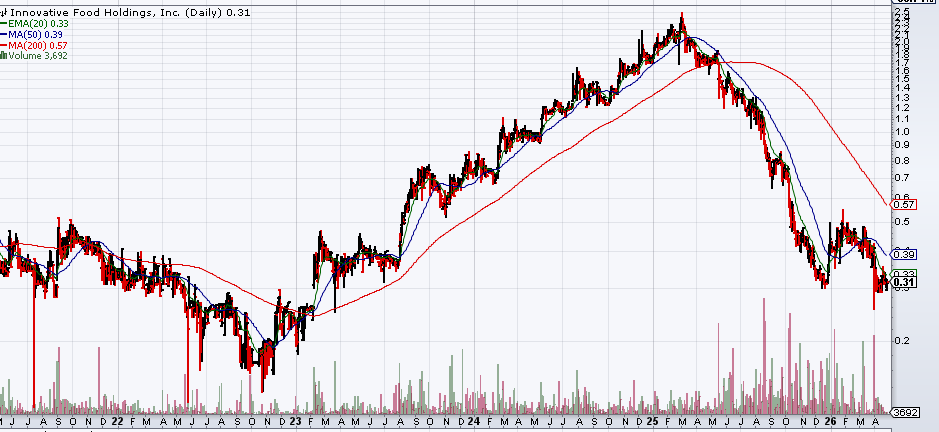

I will attach a screenshot of the company’s 5-year stock performance, and the story becomes a bit more dark. So you might ask yourself, how did this perfect setup fail?

At first, execution was actually going quite well, which was also reflected in the stock price. And the execution was already underway. Money-losing D2C brands like igourmet.com and mouth.com were being sold off, SG&A was being cut, and new customers like Gate Gourmet and Sam’s Club were coming online and supposedly diversifying revenue away from the US Foods concentration. By the second half of 2024, the stock had roughly tripled off the lows and was trading between $1.20 and $2.00. The stock started appearing on every microcap investor’s timeline, Greystone Capital wrote it up as well, so it looked like the thesis was working.

And this is precisely the moment the trap closed, because Q1 2025 looked great on the surface but contained the pattern that would define the entire next year. In Q1 2025, revenue was up 26%, which looks strong at first. But the 10q itself showed that organic growth was 22.9% and that the national distribution segment had grown 133%, with $2.0 million of that coming directly from the new acquisitions. Even more importantly, GAAP net income flipped to a loss of $0.4 million. This was the first full quarter operating with the expanded footprint, and the company couldn’t make money on it. That’s the signal that everyone, including me reading it now in hindsight, should have caught. Acquisitions were padding revenue, but the underlying business was already slipping and the new operational complexity was eating into profits.

By q3 2025, revenue grew 3.5%, but every dollar of that growth came from acquisitions. The local distribution segment grew 33% on paper but declined 21.5% organically. Digital channels declined 4.5%, with management attributing it to “continued softness with our largest digital partner,” which was US Foods, and this was also the very customer the original thesis had assumed was stabilized. Adjusted EBITDA fell from $1.0 million to $ 321K, a 70% decline on rising revenue, and cash dropped to $ 684K.

A few weeks later in October 2025, Bennett resigned. CFO Gary Schubert took over, and three long sitting board members departed at the same time. Schubert’s framing in his first earnings release was unusually direct: he said that “2025 exposed the gap between the complexity of the enterprise and the architecture supporting it.” When a transformation CEO leaves before the transformation is proven out, the next quarter almost always contains the trailing details, and that is exactly what q4 2025 delivered. Revenue was down 18.1%, with digital channels off 13.4%, national distribution off 14.1%, and local distribution off 32.3%. Cash was satting at $ 927K. The Pennsylvania facility, which was originally framed as the value-unlocking catalyst I talked about in the beginning, was sold for $9.2 million and used to pay down debt rather than to fund growth. The catalyst had become a liquidity event, and the stock hit $0.30 in January 2026, and it still trades at that level as I am writing this.

When I work backward through the data, I see five distinct variables that broke the thesis, and I think each one generalizes well beyond IVFH.

The first is that the concentration risk was repackaged rather than solved. The bull case in early 2024 leaned heavily on the idea that new partners had diversified the company away from their main customer, US Foods. The 10-K shows US Foods declining from 48% to 43% of revenue between 2023 and 2024, which is meaningful, but it still leaves a single customer holding nearly half the business hostage. When that customer’s volumes softened in 2025, the dropship business, which was the moaty part of the company, softened right along with it. Diversification at the margin is not the same as resolving concentration risk, and it’s worth being skeptical whenever management or a write-up frames it that way.

The second is that acquisitions masked organic decline for three consecutive quarters. Golden Organics and LoCo together added several million dollars to the top line, which kept reported growth positive while organic performance was already turning negative. This is one of the most common dangerous patterns in microcaps, and it’s frustratingly easy to miss because the headline numbers look fine. If a company is doing M&A, you really have to track organic growth separately every single quarter, because reported growth is the transaction layer and not the business layer.

The third is that operational complexity outran the systems infrastructure. By mid 2025, IVFH was simultaneously integrating two acquisitions, ramping a national retail channel, running three warehouses across three states, divesting the cheese business, and trying to diversify its dropship partners. For an asset-light model where margins should expand as you scale, the fact that margins compressed instead is the tell. The infrastructure couldn’t absorb what management was building on top of it, and Schubert eventually said as much directly.

The fourth is that the $1 billion revenue ambition was in hindsight a tell. A company doing $60–72 million in revenue does not credibly path to $1 billion without becoming a fundamentally different business. The aspiration itself isn’t really the problem though. The problem is that it justifies elevated spend, faster M&A, and operational complexity that the current business can’t carry. When the framing shifts, the bet you originally made is no longer the bet you’re holding, and that deserves a fresh underwrite.

The fifth and final pattern is that the CEO left before the proof. Bennett resigned in October 2025, and the worst quarter in the company’s recent history was reported about six weeks later. The pattern of such a figure leaving and the successor taking the kitchen sink is reliable enough that I think it should be treated as a base case rather than a surprise.

I think this case is the perfect example of how perfect setups in microcap’s can invert. It is our task to learn from them, and act accordingly. See you at the next edition!

The best article ever written in substack's history.